Trade tensions between the U.S and China have been rising since the U.S. imposed a 25% tariff on approximately $34 billion of Chinese goods July 6 and on an additional $16 billion of Chinese imports August 23. China retaliated each time with tariffs on approximately the same value of imports from the U.S. Subsequently the U.S. announced a plan to impose 10% tariffs on an additional $267 billion of Chinese imports. These new proposed tariffs are to be implemented in several stages depending the response by China with the ultimate expected tariff of 25%.

On September 18, China announced that it will retaliate with additional tariffs on $60 billion worth of U.S. goods with tariff rates from 5% to 10%. Note that this time China did not propose an equivalent amount of imports from the U.S. to be subject to the retaliation for two reasons. First, there are goods that China wishes to acquire from the U.S. that it does not want to tax, and second China only imported $130 billion of U.S. goods in 2017. China did indicate that there is a possibility of expanding their response in this tit-for-tat trade dispute with other non-tariff restrictions on U.S. companies doing business in China and potentially restricting exports of intermediate goods to U.S. manufacturers. China has also filed a grievance with the WTO against the U.S. claiming that the tariffs are a violation of WTO international trading agreements.

Were the additional tariffs to be imposed and the trade dispute escalated, the end-game would not be obvious. The most optimistic scenario is that the escalation stops, both sides declare a win, and both sides pull back through negotiations. There is a pathway to this result. China has been moving towards increased IP protection, and this is an issue for the U.S. In response to a deal on IP, both sides could declare victory and begin to remove the tariffs.

The most pessimistic scenario is that the rhetoric from both Beijing and Washington translates into further escalation. This narrative is fed by news organization in each country which report that the other side is feeling the pain more than they are. This end-game could well be autarky—the cessation of most trade between the two countries. There is much room between the most optimistic and the most pessimistic scenarios for a settlement. However, the political landscapes in the two countries may dictate a solution that does not correspond to the most advantageous economic solution.

In other recent trade disputes involving the U.S., there has been a more rapid movement to the negotiating table. Why have China/U.S. economic relations not taken the same path as yet? The fact is that the issues between the U.S. and Mexico; the U.S. and South Korea, and the U.S. and Europe are quite different than that of the U.S. and China. In the former, small revisions in trading arrangements, revisions that reflect changes in the world economy over the past few years, have been acceptable to both sides. As explained in our annual essay1, the issues between China and the U.S. are about fundamental domestic economic policy and about relative economic power.

In recent days, the U.S. requested a return to the negotiating table. This is encouraging news in that it follows a pattern similar to the negotiations between Mexico and the United States. Those began with strong rhetoric, met with internal opposition, and ended with the outlines of a yet to be ratified, modified agreement. The reports from Washington on the dispute with China indicate there are two camps with the hardliner camp less influential at the moment. Similar reports of controversy over strategy are coming out of Beijing. Thus, the assumption we at The UCLA Anderson Forecast have been making with respect to U.S. trade for our forecast exercise, that no major changes will take place, may well prove prescient. In this regard it is instructive to briefly review the recent outcome of those U.S./Mexico talks.

On August 27, the U.S. and Mexico reached an agreement to modernize the 24-year-old NAFTA. According to Office of the United States Trade Representative2, the agreement provides more comprehensive enforcement provisions on intellectual property, stronger standards on trade secrets, and new protections for innovators. The agreement also modernizes some of the digital products trading arrangements, products that were not contemplated in the 1980’s and 90’s when NAFTA was originally negotiated. This agreement has mutual benefits for both countries and does not disrupt the most important aspect of U.S./Mexico trade, that of automobiles and auto parts.

Can a similar kind of agreement be reached between the U.S. and China? The sticking points thus far have been the insistence by the U.S. that China change its fundamental economic policy on the one hand and the insistence by China that the U.S. cease spending more than it earns if it wants lower trade deficits on the other. Since neither are likely to happen, domestic pressures in the two countries could well make them fade away as in the U.S./Mexico negotiations with that check that Mexico will never write for a border wall.

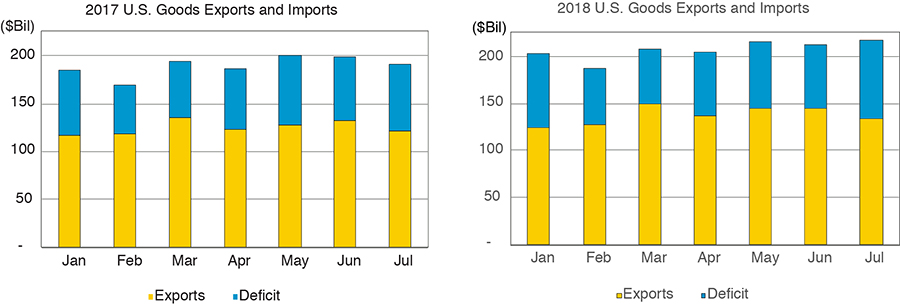

Since the beginning of 2018, the U.S. has moved to implement tariffs and to pressure its trading partners to negotiate new trade agreements. How did this impact U.S. exports and imports? Figure 1 displays the value of U.S. nominal exports and imports of goods from January to July in 2017 and 2018. The yellow bar represents the value of exports, and the yellow plus the blue bar the value of imports. The difference, the blue bar, is the trade deficit.

The good news is that U.S. trade with the world was not disrupted amid the rising trade tensions. From the graph we see there are no significant changes from 2017 to 2018. What is also true is that U.S. trade deficits, deficits that policy makers in Washington want to reduce, remain significant. The U.S. trade deficit for both goods and services was $316 billion for the first 7 months in 2017, and it increased to $338 billion for the same period in 2018. The trade in goods deficit increased from $464 billion in 2017 to $497 billion in 2018 and the trade in services surplus increased from $148 billion to $159 billion in the same period. Given the ballooning U.S. Federal deficit, we can expect this pattern to continue whether or not the trade deficit with China diminishes.

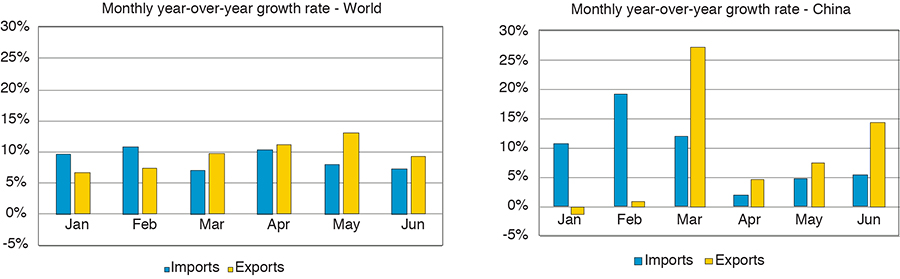

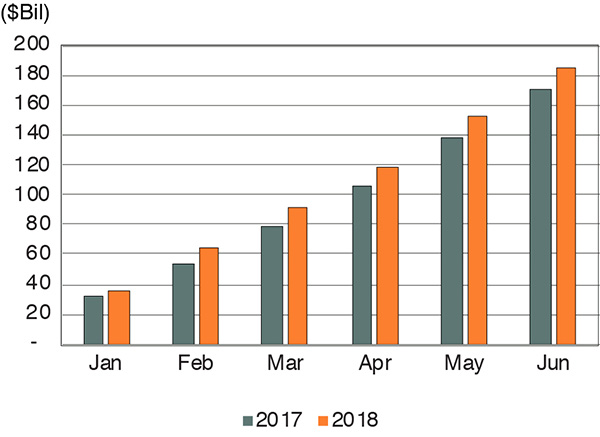

In order to see if there are any short-term reactions to the rising trade tensions and the imposition of specific tariffs, consider Figure 2. These show the monthly year-over-year growth rates of U.S. imports and exports with the world and with China for the first six months of the last two years. With the world, U.S. import and export growth seem to be stable, around 9% year-over-year. This resulted in an expected widening of the aggregate trade deficit. With China, the import growth rate declined significantly, while the growth of U.S. exports increased. Nevertheless, the disparity between the value of imports to the U.S. and to China still resulted in a widening of the bilateral trade deficit. Figure 3 shows the cumulative U.S. goods trade deficit with China from January to June, in 2017 and 2018. As of June in 2018, the trade deficit amounted to $186 billion, higher than the $171 billion deficit in June 2017.

China’s aforementioned retaliation focused on U.S. agriculture exports. As a result, some U.S. farmers, such as producers of soybeans, have indicated a loss due to the tariffs. In response, on August 27 the U.S. Department of Agriculture said it would begin compensating some farm operators for those losses. Other sectors as well as those associated with processing and transporting agricultural products have lobbied against the U.S. tariffs claiming a business impact from the Chinese tariffs on U.S. goods and services.

It is more difficult to ascertain the impact across the Pacific. However, Chinese investors seem to be nervous about the trade tensions as well as other macroeconomic issues in China. That unsettled confidence has been reflected in equity markets. For example, the Shanghai stock market index declined by 20% since the beginning of 2018, China’s foreign direct investment (FDI) to the U.S. plummeted during the first two quarters in 2018 ($2 billion compared to $29 billion in the whole year of 2017). One would expect these impacts would induce more negotiating room on both sides of the Pacific.

As the data show, we have not seen a significant change in U.S.- China trade in the first 6 months of 2018. The last few months have seen shifts in buying due to anticipation of tariffs, however after adjusting for seasonality, there is no discernable trend in either international sea or air cargo shipments. With the first wave of tariffs imposed on July 6, we expect to see a response in the trade volumes in the future. If the tariffs are binding and reduce U.S./China trade, then there will be a reallocation of resources away from trading sectors in both countries. However, the escalation of trade tensions between the U.S. and China over the last few months have as yet not engendered sizable dislocations in either economy.

Cathay Bank has established a sponsorship relationship with UCLA Anderson Forecast to produce a U.S.-China Economic Report. In this report, UCLA Anderson Forecast will talk about their view of economic analysis and perspective on the current and future outlook relating to the two largest economies in the world – the United States and China.

UCLA Anderson Forecast has been the leading independent economic forecast of both the U.S. and California economies for over 65 years. The annual report and quarterly columns written by UCLA Anderson Forecast will focus on current topics affecting investment flows and associated economic events between China and the United States.

This report includes forecasts, projections and other predictive statements that represent UCLA Anderson Forecast’s economic analysis and perspective on the current state and future outlook of the economies of The United States and China in light of currently available information. These forecasts are based on industry trends and other factors, and they involve risks, variables and uncertainties. This information is given in summary form and does not purport to be complete. Information in this report should not be considered as advice or a recommendation to you or your business in relation to taking a particular course of action and does not take into account your particular business objectives, financial situation or needs.

Readers are cautioned not to place undue reliance on the forward-looking statements in this report. UCLA Anderson Forecast does not undertake any obligation to publicly release the result of any revisions to these forward-looking statements to reflect the occurrence of unanticipated events or circumstances after the date of this report. While due care has been used in the preparation of forecast information, actual results may vary in a materially positive or negative manner. Forecasts and hypothetical examples are subject to uncertainty and contingencies outside UCLA Anderson Forecast’s control.

Jerry Nickelsburg joined the UCLA’s Anderson School of Management and The Anderson Forecast in 2006. Since 2017 he has been the Director of The Anderson Forecast. He teaches economics in the MBA program with a focus on Business Forecasting and on Asian economies. He has a Ph.D. in economics from the University of Minnesota and studied at The Virginia Military Institute and George Washington University. He is widely published and cited on issues related to economics and public policy.

William Yu joined the UCLA Anderson Forecast in 2011 as an economist. At Forecast he focuses on the economic modeling, forecasting and Los Angeles economy. He also conducts research and forecast on China’s economy, and its relationship with the US economy. His research interests include a wide range of economic and financial issues, such as time series econometrics, data analytics, stock, bond, real estate, and commodity price dynamics, human capital, and innovation.